As insurance gets harder to buy, NZ has 3 choices for disaster recovery – and we keep choosing the worst one

- Written by Ilan Noy, Chair in the Economics of Disasters and Climate Change, Te Herenga Waka — Victoria University of Wellington

The number of climate change-related extreme weather events is on the rise, making it harder for many people to buy affordable home insurance.

The industry has already signalled it is pulling out of some places in Aotearoa New Zealand, leaving the government and homeowners to question what happens next. This is not something that should be ignored, or met with ad-hoc, unplanned responses.

Since insurance is required for residential mortgages, the retreat of insurance companies will have significant consequences for property prices and local economies.

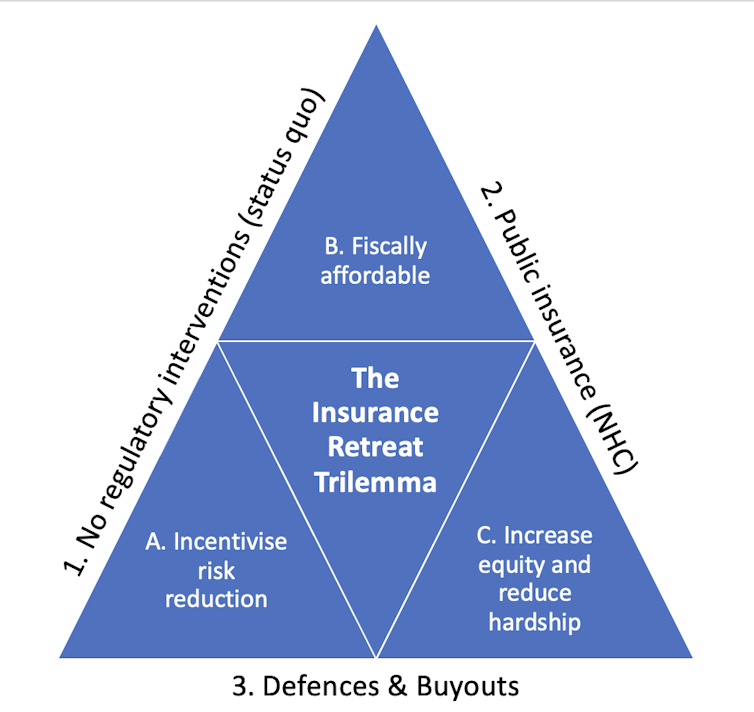

With the retreat of insurance companies a future certainty in some communities, the government must decide how to respond. In our new research), we developed the “trilemma” framework, outlining the policy trade-offs governments face in adapting to climate change.

Deciding between trade-offs

We found effective adaptation policy needs to achieve three goals:

- incentivise risk reduction

- be fiscally affordable

- increase equity and wellbeing and reduce hardship.

But any policy can satisfy only two of these three goals. The government has to make trade-offs.

When it comes to responding to the retreat of private insurance, the options include:

- doing nothing and letting “the market” adjust (with sharp price declines for affected properties)

- replacing private insurance with a publicly-funded alternative

- offering government-funded defences (for example, stopbanks) or buyouts to properties that can no longer be insured.

Each one of these options involves giving up on at least one of the three policy goals.

A world without private insurance

Let us consider “Macondo”, a hypothetical community in a flood-prone area where insurance has “retreated”.

Do nothing

The “do nothing” option is when the government does not take a policy position on flood or storm insurance. This option has little to no cost for the government and, as long as people don’t expect buyouts, would incentivise risk reduction. But it leaves homeowners completely exposed to the increasing risk.

In “Macondo”, some homeowners will have reduced the risk for their own properties (raising their houses, for example). Others won’t be able to do so and remain completely at the mercy of the elements.

Those whose houses have been deemed uninsurable would have their mortgages automatically put into default. Some may have to sell their home at a much lower price and may remain indebted even after the sale.

Local councils might offer to invest in defences for the community by building stopbanks, but that is less likely for poorer and smaller local councils.

When an extreme weather event does happen, causing significant losses, the uninsured who own their homes may be unable to repair or rebuild and will be left destitute.

Public replacement insurance

In 1945, New Zealand’s government introduced public insurance for some natural hazards with the Earthquake and War Damage Commission. This later became the Earthquake Commission (EQC), and more recently, the Natural Hazards Commission (NHC). The commission was established as private insurers withdrew earthquake cover in the 1940s and landslip cover in the 1980s.

The government could choose to extend NHC policies to fully cover weather events such as floods and storms (NHC now provides only partial cover for damage to land from these hazards). Or it could establish a different public insurance scheme to cover these hazards.

When designed well, this option makes fiscal sense. For example, after 2010-2011 Christchurch earthquakes EQC cover for residential properties didn’t carry extra costs for the government.

Public replacement insurance could also make recovery fairer for everyone. But providing a blanket safety net through a public insurance scheme would discourage risk reduction. With the greater sense of financial safety may come a higher appetite to build on more risky sites, and spend less to defend existing homes. This would result in even more exposure and more damage.

Publicly-funded defences and buyouts

Successive governments across a range of disasters have opted for the ad-hoc approach. This inevitably turns out to be a combination of publicly-funded defences with generously provisioned buyouts.

This combination of defences and buyouts may be the most politically appealing in the short term, but it is also the least affordable and the least efficient option. This option leads to reduced risk (especially if buyouts are used) and can lessen hardship and even inequities.

This policy was used in Westport after its damaging floods in 2021 and 2022. Similarly, the Auckland Anniversary Flood and Cyclone Gabrielle triggered large investments in buyouts and in new flood defences that will end up costing billions.

Unfortunately for the affected residents in both cases, the process was not done preemptively following a carefully designed process. Instead, the response to each event was designed on the fly, was lengthy, and full of frustrating uncertainties, missteps, and missed opportunities.

Proactive response needed

Currently, every successive government in New Zealand chooses to do nothing and then switches to a defence and buyout choice when disaster strikes. This is the worst of all the trilemma policy options.

A more proactive policy, even if well-conceived, cannot achieve all three of the goals we listed. But at least the choice between these trade-offs would be clear and transparent. It would also avoid all the inefficiencies created by the reactive policy choices our elected governments make now.

We are grateful for the contribution of science writer Jo-Anne Hazel to this analysis.

Authors: Ilan Noy, Chair in the Economics of Disasters and Climate Change, Te Herenga Waka — Victoria University of Wellington